Introduction

We're a very design-centric firm, but part of design is a deeper understanding of concepts at work. That sometimes leads us a bit further afield than "look at this pretty picture" into the realm of numbers and analysis. The intersection of design, home ownership, and economics is an interesting one. First, let's talk about economics and owning a house, then we'll look at ties between design and the latter two concepts in a future post. Homeownership has declined nation-wide in the past several decades. As owning a home remains a dream of many and the level of homeownership is viewed as an indication of economic conditions, this is an important metric. We're going to evaluate that situation from the construction and real estate side.

The Data

The Texas A&M Real Estate Center tracks and compiles a huge amount of information about home sales in a number of Texas's largest markets. They've got everything from number of sales, to average price, to listings, to inventory (in months -- this last obviously involves some assumptions). For this analysis, we're going to look at median price. See more in about that in the last section; in short, it represents what a prototypical homebuyer actually paid.

Now, median price is reported as it was recorded in listings of the time, meaning that data from October 1990 can't be compared directly to data of June 2016. A dollar in 1990 bought a lot more than a dollar does today due to inflation. Fortunately, the federal government tracks inflation very carefully because it impacts a huge number of conditions across the economy. We'll correct our home sales data using the Consumer Price Index, or CPI, for all urban consumers (the CPI-U, for you wonks out there).

The Graph

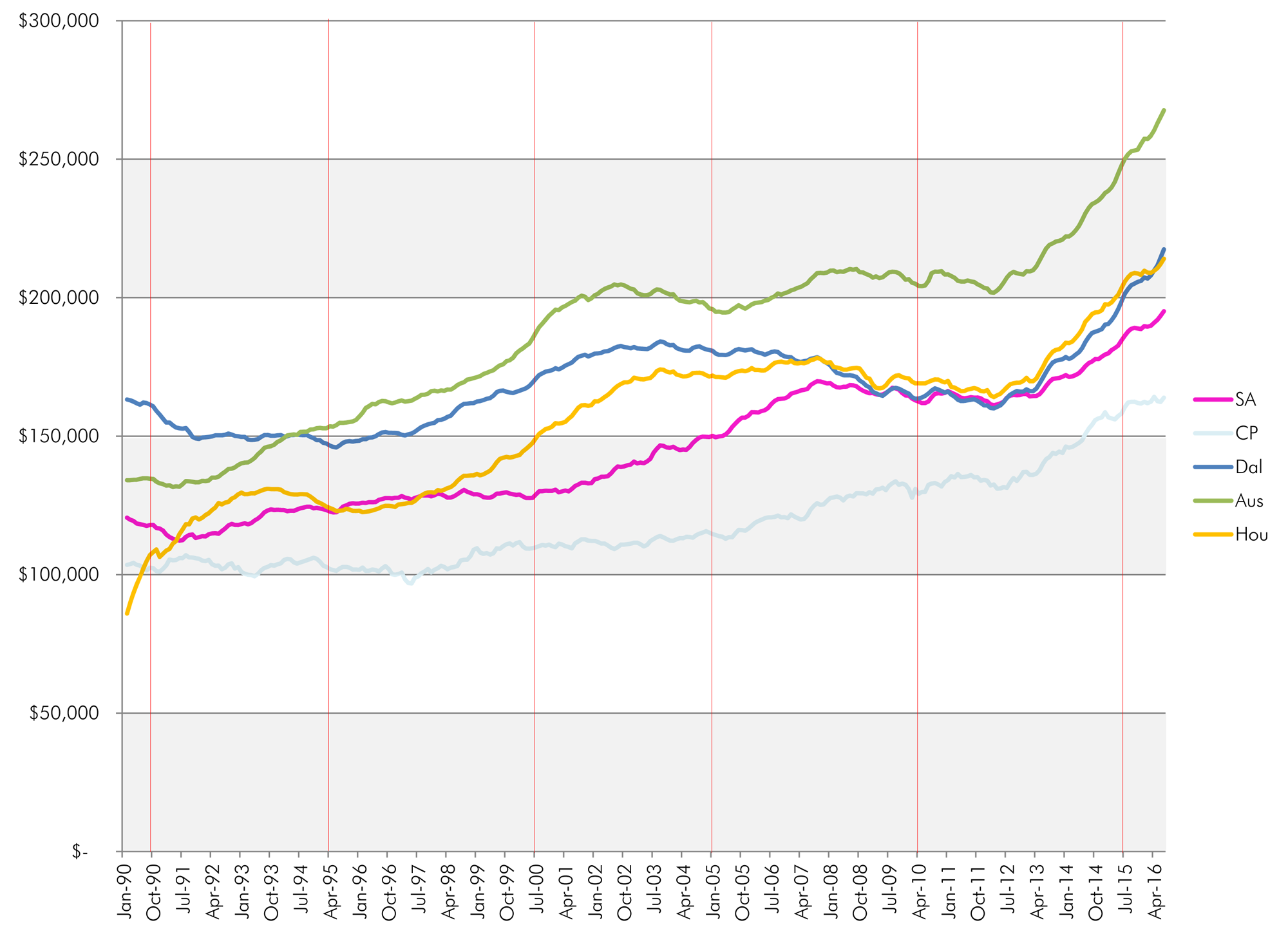

On to the graph. There are a lot of data points there, so let's talk it through a bit. First, note that each differently-colored line represents a different city. I've selected San Antonio (Fiesta magenta), Dallas (Cowboys blue), Houston (Astros orange), Corpus Christi (ocean blue), and Austin (puke green, just because).

With a little history in mind, the graph looks pretty interesting. A few points for example:

• Dallas and Houston home prices were very divergent in 1990, both saw dips after the savings and loan crisis in the mid-90s, but then Houston gradually recovered to catch Dallas. Both were affected by the 2008 housing crash as well. Both are seeing home price appreciation greater than San Antonio.

• Austin. Wow. This is one of those classic "if I'd only bought before XXXX, I'd be a millionaire" kind of graphs. Austin started the 90s as the sleepy, quirky college/capitol town we all loved, and now it's turned into the place everyone wants to be except for the fact that everyone wants to be there.

• Corpus has been slowly, steadily moving forward. The years since about 2011 are the most dramatic appreciation it's seen in this near 30-year swath of history.

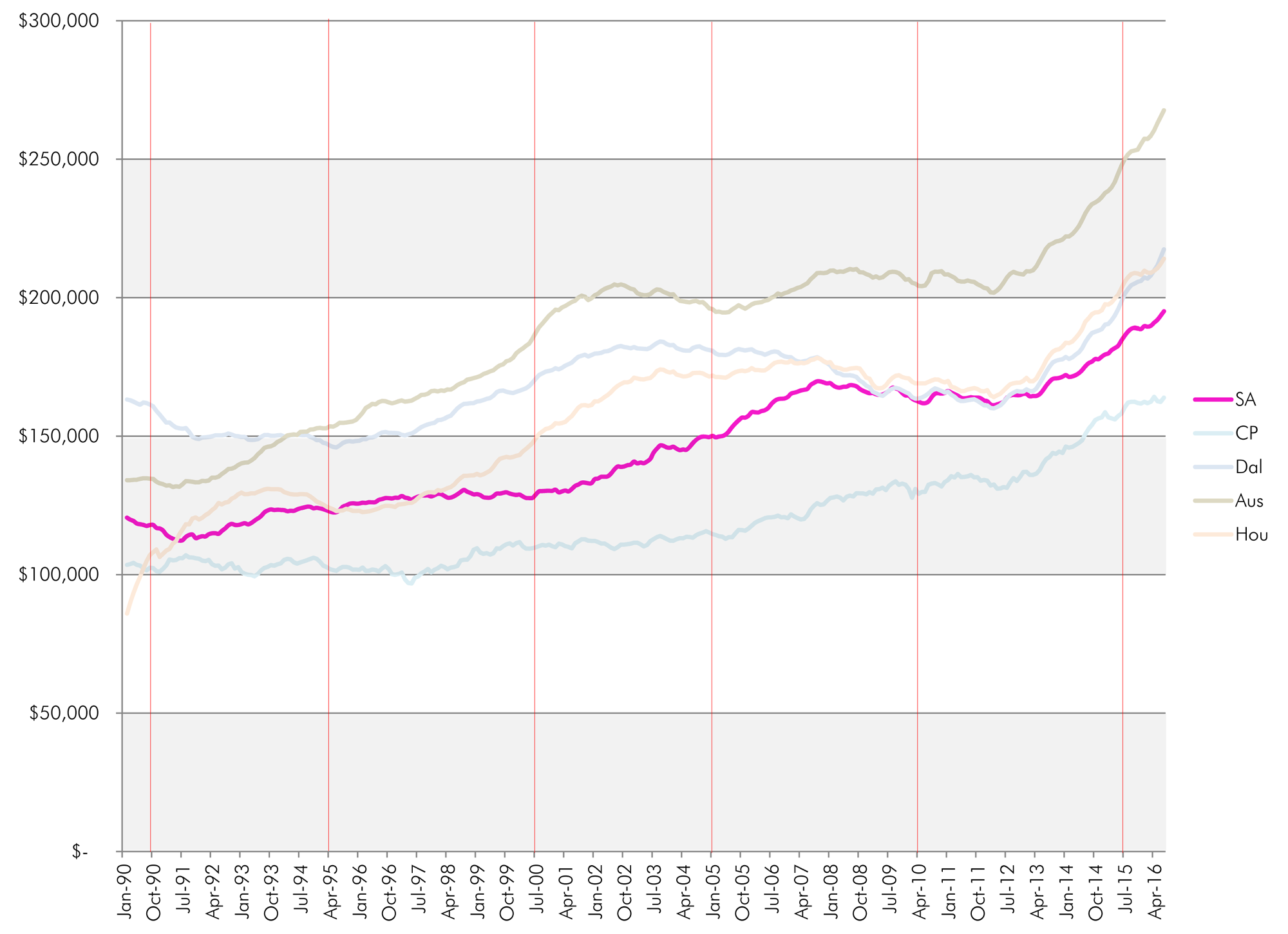

San Antonio, Specifically

Let's focus in on San Antonio. You can see a few things pretty clearly. First, San Antonio has seen a long, steady rise in prices. From the dip in 1992, all the way through, say, 2005 or so, the market didn't boom or bust. There were some sharper ups and a few downs, but by and large, it was pretty stable.

The second thing of note is that recent crash. Again, San Antonio's legendary stability shines through. You can see the (relatively) rapid increases in values 2005 through 2008. After that, things declined a bit, but they weren't huge. More of a flat trend from 2008 through 2012, actually. Not such a bad deal when other markets saw declines of up to 50%. Who's boring NOW, Las Vegas? Maybe still us. But we didn't get foreclosed, so there's that.

And the third? We're on a roller coaster headed up right now, just like everyone else. It looks a lot like the pre-2009 years, just moreso. We're on a sharper upwards trendline and it's been pretty well sustained at this point -- since 2013, we're up about 20%. We're not ones to speculate too much, but keep in mind that downs follow ups.

Further Analysis

There's another layer of analysis to be had here as well. These prices are inflation-corrected, remember? So we can make apples-to-apples comparisons between 1990 and 2016. Used to be, the middle of the market was $125,000 in today's dollars. Today, it's approaching $200,000. However, that doesn't mean that precisely the same home which cost the equivalent of $125,000 in 1990 now costs $200,000. Let's work through the factors.

• Most significantly, new homes are bigger now. The median size of a new home was about 2,080 square feet in 1990. It's about 2,500 square feet now. That's a 20% increase, but keep in mind that the graph contains both new and older homes, so that 20% doesn't translate directly

• Mechanical systems (air conditioning, heating) are more sophisticated and expensive now

• There's some evidence that expectations regarding the level of finish are higher now than in previous decades

• In some markets -- including most Texas markets -- the demand for construction has pushed up costs significantly, and potentially temporarily

What Does This Mean?

So what does this mean? Well, homeownership has decreased, for one. Rates have declined from the 68% range as recently as 2007-2008, down to the 63% range this year. Much of this is attributable to the housing crash; in addition to the well-documented causes of the crash (and foreclosure explosion), homeowners at the bottom of the range have been forced out in the past few years by loss of income due to high unemployment (though this is a much smaller phenomenon in Texas than nationwide). The higher cost of homeownership obviously makes this entire equation more challenging. Also, as interest in urban living rises (especially among millenials and baby boomers), there's been some shift to renting rather than owning, simply because of the availability and price of housing types in those areas.

So if the primary increase in home costs is due to an increase in home sizes, and that translates into lower homeownership, perhaps part of the answer is to return to smaller home sizes. Sounds like a topic for another article.

The Fine Print

A few disclaimers. This isn't a statistically valid study; we're designers, not economists. But we're not looking for scientifically rigorous conclusions here; we're looking in general at home prices and trying to see if there's anything we can learn in general. Plus, the data was assembled by Aggies. No guarantees there.

Note that the data looks at average home sale prices, not average home values. There's a difference: back in 2009, when everything crashed, more people decided to avoid selling because prices had declined and there was turmoil in the mortgage market, thereby constricting supply somewhat. If people tried to sell in 2009 at the same overall rate as in an "average" year, prices would have likely fallen further.

These datasets look at large areas. If you live in certain parts of any of these cities, you've seen significantly more appreciation in your home value than average. There are also certainly areas which have seen less appreciation than typical.

For this analysis, we've used median price. That's the price of the home in the very middle of the price range of all homes -- not the average (or mean) price, which sums up all prices and divides by the number of sales. The idea is that we're looking for a number which best represents what a typical homebuyer paid. Deciding whether to use mean or median in a particular analysis is optimally determined via a statistical approach, for which we don't have sufficient data in this case. But data sets like this one tend to have outliers -- very expensive homes or very cheap homes -- which don't represent the average homebuyer very well. Data sets with outliers tend to be better represented by medians, rather than by means. So that's what we chose.

Last, when we're trying to impute reason to these trends, it gets a bit hairy without much more in-depth study and data analysis than I'm qualified to conduct. We know some trends and events through others' work, and the basics of history. But there's more complexity to the market in any given year than the headlines will yield. Just look at this as an overview and understand that there's more depth than that.